In the 3rd chapter of the book “The Most Important Thing”, Mr. Howard Marks has discussed regarding different ways to identify the value of any business.

We always make an investment at a lower price with the intention to sell it at a higher price. Means that we buy something at less price than we can able to sell.

But what is high, price and what is a low price? How to identify it? That is the main confusion for all of us.

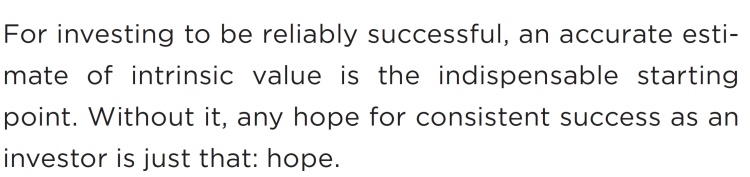

For taking it at a simplify manner, we can say that we buy at below the intrinsic value of any assets for selling that asset at a higher price.

“Intrinsic value is the value (i.e. what the company is really worth). Different investors use different techniques to calculate intrinsic value.” – InvestorWords

Now the question is how to identify an intrinsic value? As we all know that there is a major 2 discipline to identify an intrinsic value of the company’s securities.

1) Fundamental Analysis and,

2) Technical Analysis

Technical Analysis basically studies past behavior of price and from that past behavior, person predicts future price behavior.

I am not going to discuss this study in details because it’s not suitable to me and I am not able to make decisions based on past price behavior.

Move forward to the Fundamental Analysis, which is suitable for me and am comfortable with it. But again, a Fundamental Analysis also having two approaches to making a decision for an intrinsic value.

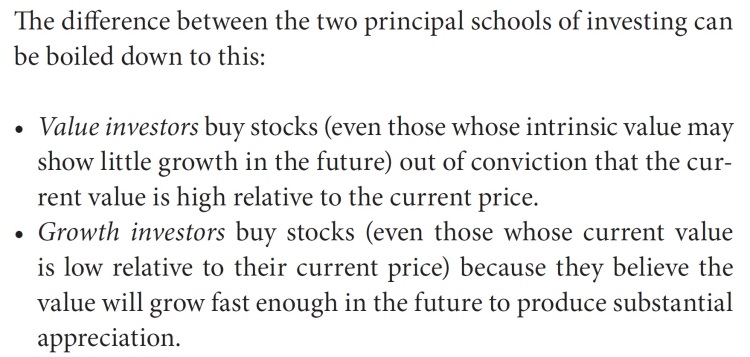

1) Value Investing and

2) Growth Investing

We need to Valuing a company by depending on a finance resource, management, business, plants & machines, factories, intellectual properties, human resources, brand name, etc.; which all having a potential to grow earnings of the particular company. And that is what we study into the fundamental analysis.

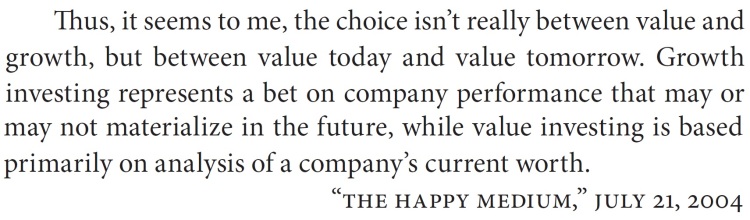

Then what is the main difference between value investing and growth investing?

Now, let me talk about the concept of valuing the company through value investing approach.

Value Investing generally focuses on tangible assets, current earnings, cash flow for valuing a company. This concept gives less weight to the intangible assets such as human resources with talents, future growth prospects, etc.

Value Investing focus on buying a company at a cheaper value based on its financial metrics such as current earnings, cash flow, dividends, tangible assets and enterprise value. Value Investors qualify the current value of the company and buy it when the current value is much higher than trading price.

Value Investing is also known as “net-net investing” approach, where investors try to identify the company which is available at below its current asset value.

Whereas growth investing focuses on to identifying companies which having a very bright future growth prospects. Here, no focus on the current value of the company and also given more weight to the intangible assets.

Still having a confusion for selecting an approach for determining a value of the company.

If we have bought a security of a company which is available at cheaper than the current price, but at the operational level, the company is not able to do well enough, then that value cannot able to remain sustainable for the longer period of time. The value will get decompound rather than be getting compounded in the future. And that increases our probability of incurring the loss.

I read one wonderful article about the value trap company.

The company looks very cheap on the basis of the financial metrics, but if someone who do not have paid attention to the business of the company then—

An investor has lost his capital also. So, that in value investing also, we cannot escape from the future. (For detail article, Kindly visit – http://neerajmarathe.blogspot.in/2010/04/mtnl-value-trap.html)

For the growth investing

But is it such easier to perform?

Let me take an example of one the biggest wealth creator company of the Indian stock market—

If someone has bought this company during the March-2000, At the high price of around Rs.431 then after the 16 years of the period, he gets returned at 7% CAGR. And if enter to the similar company at the low price of around Rs.275 during the March-2000 then after the 16 years of the period, he gets a returned of 10% CAGR (*Considering all time high price for calculating returns). Though revenue grown at 30% CAGR, Operating profit grown at 27% CAGR and Net profit also grown at 27% CAGR during the same period with supported by good management team. During March-2000, the company was traded at 64x P/E at low price of Rs.275 and this multiple are common now-a-days.

There is a very thin line difference between Growth investing and value investing.

Value investing is more consistent in nature, but it’s not easy to find it out. It is not an easy task to valuing a company through value investing approach. I also learn this valuable learning after made the such mistake. If we don’t able to make our estimate appropriately than we might overpay or underpay to that particular security. If we overpay for some security, then we have to take support of good luck for getting some greater fool who buys securities from us at a higher price.

Also, the most important thing is not to just valuing security appropriately, but also, we need to hold it. Stock will not start moving up after we make our purchase. Stock does not know that we are holding it.

After our purchasing, many a time price will start to fall further. But we should hold to it firmly. If something good at price X then it will be more good at price X-1.

This law of demand is not really put by investors into practice in the stock market. We tend to buy more stock when the price starts moving up. But if we have done all our work properly, then decline in the price of security should not make us uncomfortable and we should also need to add more at a lower level.

Read for more detail: The Most Important Thing Illuminated by Howard Marks

Disclaimer

Above article is just my perception, and perception can be wrong. For me, my perception can be right but for others, it might be wrong.