The second part of Series “Once a darling, now an evil”. This series is based on the companies which were once upon a time darling of the market and now, it has wiped out the majority of all those gains. I am trying to put some of the number-crunching facts by which we have identified ongoing issues in the companies and have saved our wealth.

I am starting this part with one of the agro commodity trading company which has an all-time high price of Rs.5500 and now last traded price at Rs.1.60. and high of Rs.506 and Rs.364 in the year 2008 and 2010.

What a wonderful company!!!! Look at the fixed assets turnover…

But some interesting data…

Another interesting data….

Without a payable and without keeping an inventory, the company has achieved a huge turnover. But only receivables are there….

(Data of FY07-08) This looks something susceptible…. ~10%+ advances of sales… and that reach to ~71% in FY10. Majority of the companies were investment and finance companies.

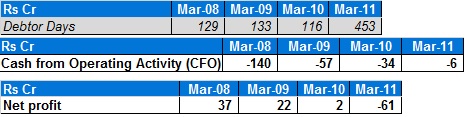

One other company which involve in the construction activities, which has an all-time high price of Rs.540 and now last traded price at Rs.0.30.

We can see that the company is into the construction business but the company does not have to keep any of the inventories.

Also, debtor days are growing and CFO is negative though the company has reported net profit. Working capital is responsible for negative CFO.

Advances recoverable is ~45% of balance sheet size in FY2010 and ~43% in FY2009. Also, the company has a contingent liability of ~Rs.725 cr which is ~96% of the entire balance sheet size, 2.27x of sales and 319x of net profit in FY10.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

We have seen a sharp fall in the market these days. Now, everyone has a question that what can be a probable bottom? where we should start buying? Bottom of the market already made? Should we buy or will we have missed out this opportunity? Yes, Nifty has reached to the fair value zone but pendulum never stayed at the middle zone it will go extreme to both the direction. So, we have seen upside extreme and now have to see downside extreme move.

Before starting answering the above questions, here, I am requesting you to read my old article which I had posted on 4th August 2019. In that article, I mentioned regarding market fall. Please first go through that article because the current article is a continuation of that article.

Now, if we analyze current fall then we can say that Indian corporate and GDP has witnessed a limited growth in the past. Also, Covid-19 virus has disrupted the entire world economy. Majority of the economy has started giving a revival package but if we look at the speed of the spreading of Covid-19 and death of the people then it is very painful for us as well as the economy.

Our PM has announced with the 21 days lockdown to fight against the Covid-19. We have taken this step well in advance so that we can able to control the situation, because if the situation will go out of control then we do not have a proper infrastructure for citizens to cure.

I have taken a few data from HDFC Bank India growth outlook 2020, cost of lockdown.

By looking at the above data and havoc of Covid-19 in the world, it is essential to go for the not only lockdown but to declare an emergency in India. Now, let’s go to the economic impact of this mayhem. People can oppose that government of the majority of the economy has started announcing a revival package. But We have to think that it’s not a financial crisis where you pump liquidity into the system and things will start recovering. It’s taking the lives of people so what will change after the liquidity get infused. People try to save life rather use those liquidities. So, disruption can take time to revive. If this problem can worsen it will be led to a financial crisis which is still pending to come. It’s just my thoughts, don’t know what can happen but this thing looking worse than any financial crisis.

If the normal situation has come where growth remains subdued then the market can remain in range but here this difficult situation can hamper the earning badly. we have to understand that our states of India are equivalent of the many of the country where corona has done huge damage. Here, the world economy gets hamper, trade around the world hamper, supply chain get disturbs, corporates have to fund fixed cost, they only can manage variable cost through the lockdown.

Many of the articles and reports indicating towards global recession and as intense as the recession of 1929. I don’t know that will happen or not but I only can pray that such will not happen because it will take many further issues with many of the lives. Let’s not getting into the debate and do some number crunching which is always my favourite.

Current, Nifty EPS is ~Rs.444 so proceed with the calculation based on that. I am assuming current EPS will remain same for FY20 and all degrowth will account in FY21 and FY22 (if the situation will not come to the control then FY22 will also go for a toss).

I have taken the bank rate as an SBI FD rate after the rate cut.

Now, if we look at the earnings yield to bond yield ratio then it has reached at the 1.03x in the current period. If we take same EPS and take that ratio to the worst happen during the 2008 – financial crisis then it was 1.11x so nifty level come to the 8000 but Covid-19 will going to hamper earning growth and might be a new level of earning yield to bond yield ratio can come, which I have taken a range of 1.25 to 1.50 with a different scenario.

If things will be in control in coming few days then might be 5% degrowth can be possible and then market also maybe get stable at the old worst level of earning yield to bond yield ratio – 1.11x to 1.25x. But if things will get more worst then now and continue with coming 1-2 months then 10% degrowth in earning can be expected. I have made a study in S&P500 of USA and in that market earning yield to bond yield ratio has reached around 3x in worst level which I am not considering as of now. If we see that then past falls in the market have accounted for ~50% fall from the top so that that will also come to ~6215 level.

Now, another point is that earnings growth always essential for generating returns in the market. So that market can be remaining in the range till no sign comes for earning growth revival because, on the hope of earnings growth, the market has already run a lot.

I have posted an article on WHAT CAN BE A PROBABLE RETURN FROM SENSEX IN COMING 10 YEARS? a way back and where I have taken SENSEX level after 10 years on worst earning growth of 3.50% came at 43547 on P/E and 57678 on P/BV based. So, if earning growth cannot revive then the market can remain in range for a longer period. But from the current base, we can have a good chance of making a return in the range of 4-7% CAGR in the index overcoming 10 years. Tax cut reform will also aid in earning growth coming forward. We only have to pray that situation will not worsen from here and for that we have to stay at home, stay safe and fight against Corona.

As an investor, we have to deal with the prices of assets and evaluate where currently its standing and what can be in the future. Prices of assets are getting affected by fundamental and psychology.

Psychology of the people does not remain the same forever. It will change for any of the reasons for millions of reasons.

Rising prices of the assets make investors’ psychology in the optimistic area and falling prices of the assets make investors’ psychology in the pessimistic area. The reason and result for the occurrence of the cycle do not remain the same with all the cycle but it is sure to a repetition of a cycle. Performance numbers are already recorded and sometimes, we require skill to understand it thoroughly. This is a past and we are not able to predict the future. It is essential to roughly think about the future to protect our investment. Second-level thinking also help us to understand the psychology of the market participants and act according to our conclusions.

There are few factors which influence and force cycle to occur.

Confirmation bias where investors seek for a piece of information or events which supports the thesis or not.

The tendency toward non-linear utility where we value a money loss is far greater than money made.

The gullibility is which influence the investors to swallow tales at good times which have the potential to gain at a good time and the excessive scepticism that makes them reject all possibility of gains in bad times.

Risk tolerance and risk aversion which investor ask for risk premium for the incremental risk.

Herd behaviour indicates to act with keep in mind that what the other people are doing.

One of the highly influential bias is to see other people making money with the idea which we have rejected initially. We do not resist such situations and left with the buying those assets which resulted in a boost to the asset bubble. Also, we generally do not select an unpopular idea and prefer to go with the herd.

All such biases lastly transform into the greed for more, envy of the money others is making, and fear of loss.

A bull market where prices of assets risen, rising or will raise and bear market where prices of assets fallen, falling or will going to fall.

But there are three-phase of the bull market –

In the first phase, growth and better improvement are invisible to most of the investors. Because it does not have a huge price appreciation, also occurs after the crash, wipeout of the prices has affected the psychology of investors.

In the last phase, prices of assets have risen, improvements are visible & started a long back. This improves the mood of the market and investors where they are ready to pay any price for the assets.

It is obvious that those who buy assets in the first phase, those got assets are at bargain prices and the probability of making money is huge. Whereas those who buy assets are at last phase then assets are available at costlier prices so that probability of losses are higher.

“What the wise man does in the beginning, the fool does in the end.”

Warren Buffett has said much the same thing even more concisely: “First the innovator, then the imitator, then the idiot.”

As we have seen three phases of a bull market, there is also a three phases bear market.

We have to see the problem behind the scene. Because an excess of good things always invites trouble. And an excess of pessimism gives birth to the new era of optimism. We need to focus on each little thing happening into the surrounding which helps us to recognize problem or opportunity earlier than others.

People always get pain when they see others are making money so that they fear continuing of trend and they will miss out on an opportunity. Thus, they also join the trend. Such influence affects the investors who have rightly enter at the first phase and by affecting the psychology, they again enter the last phase where they involve doing the wrong things. The most brilliant person also can fall under such psychological influences.

We also have to understand that the bubble is not always where the market raises and also not bust where the market falls.

If the company is good in quality then also it has taken around six years to reach the same price but if assets are not good quality then it gets disappear after the bubble get burst.

No assets are good enough that it will never be going to become overvalued. Price does not matter and borrowing money to make an investment are a sign of building a bubble. I have met a few of the people who take a loan on credit card, use credit period to trade in the market. Such is a sign of the bubble. This was an incident of late 2017 and starting of 2018.

We can see that good news, maximum availability of the credit, maximum optimism in psychology, maximum prices, minimum potential returns, etc. All come at the same time, which is a signal for the identification of the bubble.

Reversed to the top, the bottom has an inability to get credits, falling in the asset’s prices, maximum pessimism, bad news flows, minimum risk.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

I am going to start this new series with all your love and wishes. Series “Once a darling, now an evil” is based on the companies which were once upon a time darling of the market and now, it has wiped out the majority of all those gains. I am trying to put some of the number-crunching facts by which we have identified ongoing issues in the companies and have saved our wealth. This series is an extension of my previous series “Numbers tells you everything”, this series I have left in midway due to some technical issues with my database.

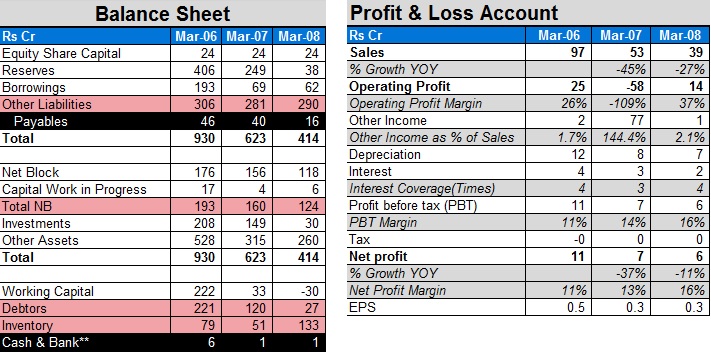

I am starting this series with one of the graphic company which has an all-time high price of Rs.2100+ and now traded at Rs.0.25. and high of Rs.13.47 in the year 2007. Due to unavailability of data prior to 2006 and unavailability of the annual report prior to 2010. I have to start showing number analysis from 2006 only.

Wow!!! What a strong cash flow from operating activities!!! From the above data, the company seems strong but….

When we look at the balance sheet with putting P&L with it then….

The company need Rs.193 cr of fixed assets to do a sale of only Rs.97 cr. Sales are just a ~10% of the entire balance sheet size. Debtors of the company were Rs.221 cr and inventory worth of Rs.79 cr compared to the sales of Rs.97 cr in FY06. Debtors were almost 2.28x of sales and inventory was 81% of sales. Look at the below data.

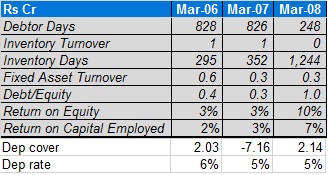

Few more interesting data…

Means when a company sell its services, the company gets payment after 828 days in FY06 and 826 days in FY07. In addition, the company takes 295 days to convert its inventory into the finished products in FY06 and that increase rapidly as COVID-19 has grown.

Now, the question is if a company has higher debtors and inventories then how CFO remains much stronger.

The answer is here. Working capital changes have contributed that boost into the CFO. If we look component of it then debtors have majorly reduced but still in FY07, debtors as a % sales remain as high as earlier due to a sharp fall in the sales.

If we have look at these basic number analyses and not deep crunching then also, we have avoided investment into such company and have saved our wealth. I have not talked about the company’s investment worth of ~Rs.130 cr in its subsidiaries in FY10 and both the subsidiaries are located at Mauritius. Also, ~Rs.134 cr of advances recoverable in FY10. There are many such points but without looking at all such points, we have avoided and saved our wealth.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

We have seen the financial cycle in the post of the credit cycle. Similarly, Real Estate also follows the same cycle as all the financial cycles follow, except one that real estate having a higher lead time to development takes place. Generally, real estate projects take a huge time to get constructed to get commercializes.

When the economy is bad at that time credit will be unavailable for the construction work and when time is a good credit will available easily. This impact on the real estate cycle. Better economic time causes an increase in demand and bad economic conditions led to a fall in the demand. Due to the higher lead time, supply & demand mismatch takes place which causes the rise in the rent and the sale price.

When projects got halted due to the credit unavailability then these situations invite a bust in the Segment. That will cause a fall in the price of buildings. Investors can get land less than what developers have invested in. Also, here, lead time reduces as approval got finalised in good time. It hurts to the projects of which construction started in the boom period.

When there is a demand for home and financing options available, builders decide to build a home and all builders decide the same which creates a surplus of home. Also, due to long lead time, demand gets soften then builders left out with the inventories which he has to sell at lower than the expected value. But the reverse of it, when the economy is slow, availability of finance is low and pile-ups of unsold inventories so that builders stop building a new home. This helps to slowly getting sold out of inventories. Now, when the economy revives again, at that time supply will be lower than the demand which brings prices to the upper level. So that building a home during the slowdown is a better way to reap profits.

People tending that real estate investment beat the inflation (same for common stocks) but we need to understand that if the price which we pay are too high then it will not beat inflation and in result, it will beat us.

If we have bought real estate during a high price growth then we have to wait a little more while price growth has been slowing and many of the area it has been degrowth. So that not all price purchased of real estate result into the wealth creation.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

Mr Marks has mentioned that he has focused on the distress debt companies where he selects the company which is operationally well but having a debt-laden balance sheet. Means company has to work on reducing debt which will bring value creation for shareholders.

So that we have to analyze thoroughly to identify the value of the company and at the end of resolution what we rewarded. If after resolution amount worth higher than the currently available debt securities price then we should buy those securities. This is difficult to play in India but we can play such where a business does not have a much problem but due to some problems the company has brought debt. When the company started paying debt, we can look into it. One of the air-cooler company has a track record of success in such a strategy.

Example of failure of this strategy in India – One of the Jewelry company in India

If we see the above balance sheet then we can see that inventories of the company were higher than debt. If the company liquidate its entire inventories and pay the debt then also the company remains with excess cash. And company available below that value.

As we have seen in the credit cycle that when credit is easily available then everyone goes for it with the compromise on the standard. But when the economy starts to contract at that time, credit availability becomes tough so that debt-laden companies cannot able to refinance their existing debt. This incident brings them at the event of bankruptcy and that hurt the psychology of investors. Selling of the debt securities starts and prices falls as everyone starts avoiding it.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

A good company does not need to always remain a good investment. We have to focus on the good deal which has a good price with limited risk and potential for return is substantial.

Changes in the availability of the credit create a fluctuation among the economic activities which tends to have resulted in the economy and profits cycle. The credit cycle has an immerse important for economic development. Corporates require additional capital to grow further and unavailability of capital make it hard for them to grow.

Similar situations we have experienced recently with the financial companies where they have brought short term borrowings to support long-term lending. And their failure to the repayment of short-term borrowings has created a crisis.

The occurrence of the credit cycle

This leads to again starting the same cycle. It takes time to complete the entire cycle but it will complete for sure.

As the Economist said earlier this year, “the worst loans are made at the best of times.”

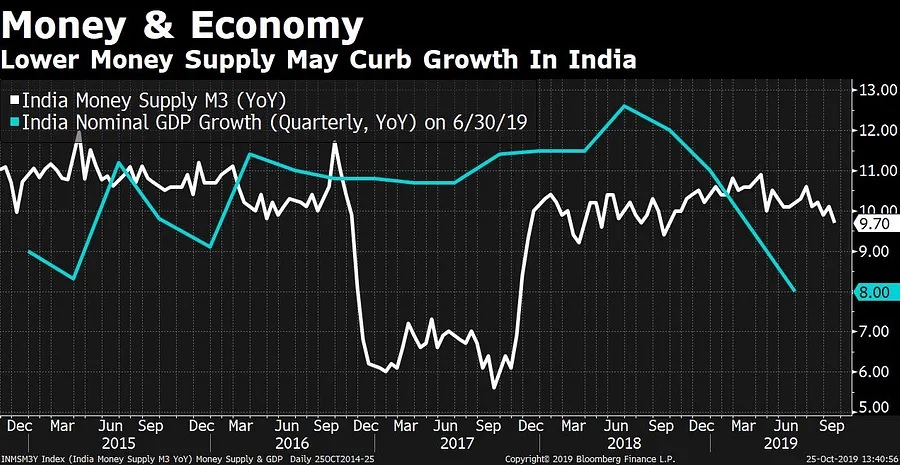

Reduction into the money supply into the economy has led to liquidity crisis and slowdown into the economy.

Money is also a commodity as other commodities so that when the competition starts getting increased, financial institutions have to make availability of money at cheaper rates. This brings down the margins of the financial institutions. Cheaper money invites to more borrowers and borrowing without discipline resulted in the huge negative consequences. When anything easily available then we do not value it particularly and that leads to destruction.

We cannot predict the time and the extent of the cycle but sure enough that cycle will going to occur and also, we can say that we are either near to occurrence or not.

It is difficult to take a call on the economy while investing but we can keep track of the supply/demand picture relating to capital. For knowing where we stand in the cycle, we need to track the credit cycle. Mast bull market getting inspired by the availability of the credit without any care for the future consequences. And the most bear market is the result of the unavailability of finance for the different projects.

When margin calls hits for the levered firms then they were forced to sell their assets or need to bring additional capital to survive. Such period forced people to sell debt securities and that will have resulted in the lower prices of debt securities. At such a lower price, yield becomes so attractive that investors can start taking buying position on it.

When we see an environment like fear of losing money, unwillingness to lend and invest regardless of merit, shortages of capital everywhere, economic contraction and difficulty refinancing debt defaults, bankruptcies and restructurings, low asset prices, high potential returns, low risk and excessive risk premiums then it is a natural time to start investing.

So that when we see these events then we have to be ready to be cautious because these events invite an increase in debt level, issuance of unsound & overpriced securities etc. These all become a starting step of a bust. When the credit cycle is in an expansion phase then we have a huge issuance of the securities that means people accepting new issuance. But extensions of it in the way of unsound & overpriced securities. Also, we heard stories like next Infosys, next Microsoft, management performing like Warren Buffett, etc. etc.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.