These are few things done by the author. We need to take action and consistently performing the same for achieving the goal. We have to learn from others, experiment those learning and has to do what is really suitable for our temperament.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

The second part of Series “Current temptation, future frustration“. This series is based on the companies which are currently darling of the market and many trying to catch such opportunities but it has a probability to become a reason for future frustration. It can wipe out the majority of gains in wealth. I am trying to put some of the number-crunching facts by which we can identify ongoing issues in the companies and can save our wealth.

I am starting this series with one of the company which is engaged in manufacturers of Wind Turbine Generators (WTGs) in India, has a 52 weeks low price of Rs.16 and LTP is Rs.48.15. This company has rewarded ~3.01x of return in a year.

Let’s start looking at the numbers.

We can see that the company has a declining trend of revenue, operating & PAT level also incurring losses. But the company has delivered a good return in a year so it might be possible that the company has a strong balance sheet.

When we look at the balance sheet then I got shocked. The company has trade payable, inventories and receivables are higher than sales. Also, the company is getting higher advances from its customer which is again higher than sales so that the company should have a monopoly and everyone wants its products only. But then why revenue keeps on declining?

Cash conversion cycle of the company is of 497 days in FY20 means its take almost 1+ years to convert to cash. Even the company has receivables, inventories and payables as a % of sales are 174%, 131% and 139% respectively.

When I have looked at the related party transaction then Rs.450 cr of sales in FY20 and Rs.648 cr of sales in FY19 done through related parties which are 59% of sales in FY20 and 45% in FY19.

Another part, when we look at the advances from customers then all are from related parties only. This trick is used by the company to show slightly better CFO. Also, receivable from related parties is 20.49% of total receivables in FY20 and 18.40% in FY19. And if we look at the receivable as a % of sales to related parties then it is 60.16% in FY20 and 46.31% in FY19. Now, I am curious that related parties have ~Rs.1100 cr of the fund to give as an advance but do not have Rs.270 cr to pay for receivables.

When we look at the exposure of the company to related parties then it is worth of Rs.865.46 cr in FY20 and Rs.708.10 cr in FY19 which is 16.35% in FY20 and 14.94% in FY19 of total balance sheet size. These related parties are making losses.

The company has Cumulative CFO < Cumulative PAT which shows difficulties to convert PAT into Cash Profit. Also, CFO is artificially boosting through advances from customers which is from the related parties.

This entire series is based on past available data and ignored the future development in companies and the stock market always looks at the future.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

There is an opportunity available, we need to train ourselves to see it. There are 10 steps mentioned by the author which he has used for creating wealth.

1) Find a reason greater than reality: the power of the spirit

There is always a reason for doing something which is a combination of what wanted to do and what we don’t want.

The author mentions that he does not want to get employed, want to get financially free which provides him with freedom of time. If our reasons do not strong enough then we do not get ready to work hard for doing a thing which we have decided to do. We should understand that without a strong reason or purpose, anything in life is hard. First, complete this step before proceeding further.

2) Make daily choices: the power of choice

We have a choice while we get a rupee. With this rupee, we can choose to become a rich, poor or a middle class through our spending habits. As we have discussed the assets and liabilities so that we need to work on increasing our assets column.

We do not have money then OK but how we spend our time, money which is our choice. We have a precious time with us and we can choose it for learning or just pass it out. As we have a single rupee and choice is us for how to use it. Similarly, we have every single minute and the choice is us how to spend it. When someone teaches us something then without getting arrogant, we need to understand why he is saying such, keep our mind open. We need to keep on learning and after that requires to make a mistake which helps us to understand it in detail. We can learn from the mistake of others. We have to invest in our greatest asset which is our mind. One or two of the successful investment does not make us a successful investor but we need to keep on learning and growing.

3) Choose friends carefully: the power of association

We should not have a friend with comparing to the financial statements, rather we have a friend by looking at their vow of becoming friends. We can learn from rich or middle-class friends also.

Many of the people have their point of view and we need to listen to them with an open mind. We can come to know something new also. We need to know what we are doing and true to ourselves. We do not have to go with the crowd for wealth building.

4) Master a formula and then learn a new one: the power of learning quickly

We have to learn many things and have to master particular things. We have to be disciplined to implement what we have learned. After master into the one learning, we need to move to another learning to master it. In the current fast-changing world, we need to learn fast otherwise our learning will be outdated.

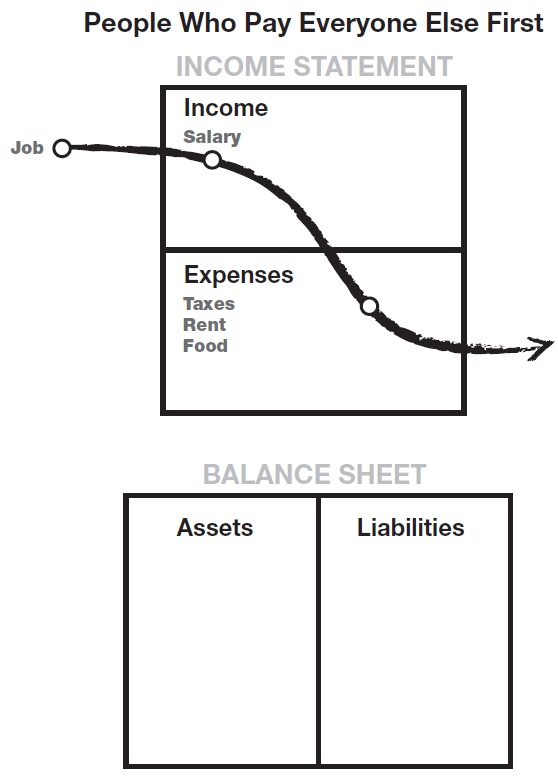

5) Pay yourself first: the power of self-discipline

If we do not have self-control, then we cannot able to become rich. Without self-discipline, lottery winner also broke.

The three most important management skills necessary to start your own business are the management of 1. Cash flow 2. People 3. Personal time

These skills help us to grow and richer but require greater self-discipline. So that pay yourself first is self-discipline and important concept.

This means what Mr Buffett has mentioned

Income – Investment = Expenses

We should not get trapped of the liabilities and if we owe liabilities then we should not work to pay for it rather others need to work to pay for it.

Rich knows that savings and investments are for creating more money, not to pay bills.

This rule does not encourage self-sacrifice or financial abstinence. It doesn’t mean to pay yourself first and starve. Life was meant to be enjoyed.

06) Pay your brokers well: the power of good advice

Many a time, we try to save cost and focus on removing intermediaries but we forget that paying well to the professional help us. They provide us with a piece of useful information and services which can help us well.

We have to separate genuine and fake professional and then appoint them as our advisers.

As we have seen that we require to have the skill to manage people. The real skill is to manage and reward the people who are smarter than you in some technical area.

07) Be an Indian giver: the power of getting something for nothing

As we all are an Indian and we people want to know how fast they get their money back.

Wise investors must look at more than ROI. They look at the assets they get for free once they get their money back. That is financial intelligence.

08) Use assets to buy luxuries: the power of focus

It seems easy to use assets column to build a cash flow but difficult in practice. When we are on a diet, many noise and temptation affect our strict actions do not follow our plan. Similarly, when we have prepared a plan to follow our investment and build assets column then outside noise and temptation to fulfil the needs going stop us. In the current environment, very easy to get a loan for any need. And that creates a temptation among us. But we should focus on the creation of the assets column rather bring liabilities on the balance sheet.

Majority of the people cannot able to master their self-discipline and that stops them from becoming rich.

I do not say that do not buy a luxury or stay away from it. But rather to buy it through the liabilities, buy it from the cash flow generated from the asset’s column. And till the time, we do not build our assets column, we have to stop our temptation.

When we have a hero, we try to become like them. And this act helps us with lots of learning. I have a hero in my investment career who are Neeraj Marathe Sir, Kuntal Shah Sir, Warren Buffett, Charlie Munger, Howard Marks, Benjamin Graham, and my friends Mr Amit Pandey, Mr Swapnil Modi. I learn from them; I look at them and try to develop skills into myself. These concepts teach me a lot. Having a hero inspire us to make a decision and act to achieve our desired goal.

10) Teach and you shall receive: the power of giving

When we want to receive something, first we need to give it to others. As a famous saying – Give respect, take respect. So, what we give, we receive it in a multifold.

So similarly, when we teach to those who want to learn then we get more learning in return. With the same mindset, I have started writing a blog so that I can distribute my learning to others and I got multifold learning over some time. I still keep distributing and keep getting back in return. And for that, I am grateful to all the readers.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

The 13th part of Series “Once a darling, now an evil”. This series is based on the companies which were once upon a time darling of the market and now, it has wiped out the majority of all those gains. I am trying to put some of the number-crunching facts by which we have identified ongoing issues in the companies and have saved our wealth.

I am starting this part with one of the company is in the business of manufacturing and trading of iron and steel products which has an all-time high price of ~Rs.443 in 2012 and now last traded price at Rs.1.59.

In the first instance this company having a huge sales growth. But PAT has huge volatility.

So, we go deeper ….

Here, we can see that debtor day and inventory days are growing rapidly and assets utilization & return ratio are falling.

I would like to go further detail of it.

Here, we can see that CFO is very volatile with cumulative CFO of FY09-12 is Rs.-20 cr whereas cumulative PAT is Rs.88 cr so that CCFO<CPAT which indicates that the company has a working capital issue which we have seen in debtor days and inventory days also.

The company shows good depreciation cover because of the capitalization of assets. One can improve depreciation cover either through improving EBIDTA or by reducing depreciation. If an asset is capitalized then it is not expensed in the same year the asset is purchased. So that here the company has selected to reduce a depreciation.

Actual Journal entry of depreciation

Depreciation A/C Dr

To Accumulated Depreciation or Fixed Assets A/C

Here, depreciation charge at income statement which will reduce the bottom-line of the company. And also added to the accumulated depreciation or directly reduces from the fixed assets so that value of fixed assets gets reduced.

But what happens when the company has decided to go for capitalization of depreciation

Fixed Assets A/C Dr

To Cash A/C

Here, the value of fixed assets gets increased rather than getting it reduced and cash will directly getting reduce with that amount. The income statement does not have any impact it which resulted in reduces depreciation expenses and improves bottom-line.

So that when the company is making a capitalization of depreciation then we have to look at the FCF rather than just check CFO. And when we go for FCF then it’s negative in all the periods. Capitalizing an expenditure enhances current profitability and increases reported cash flow from operations. Capitalization of depreciation will increase the value of assets which is not a part of CFO but it’s a part of CFI so that FCF will provide us a better picture.

Also, the company does not have any interest cover.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.